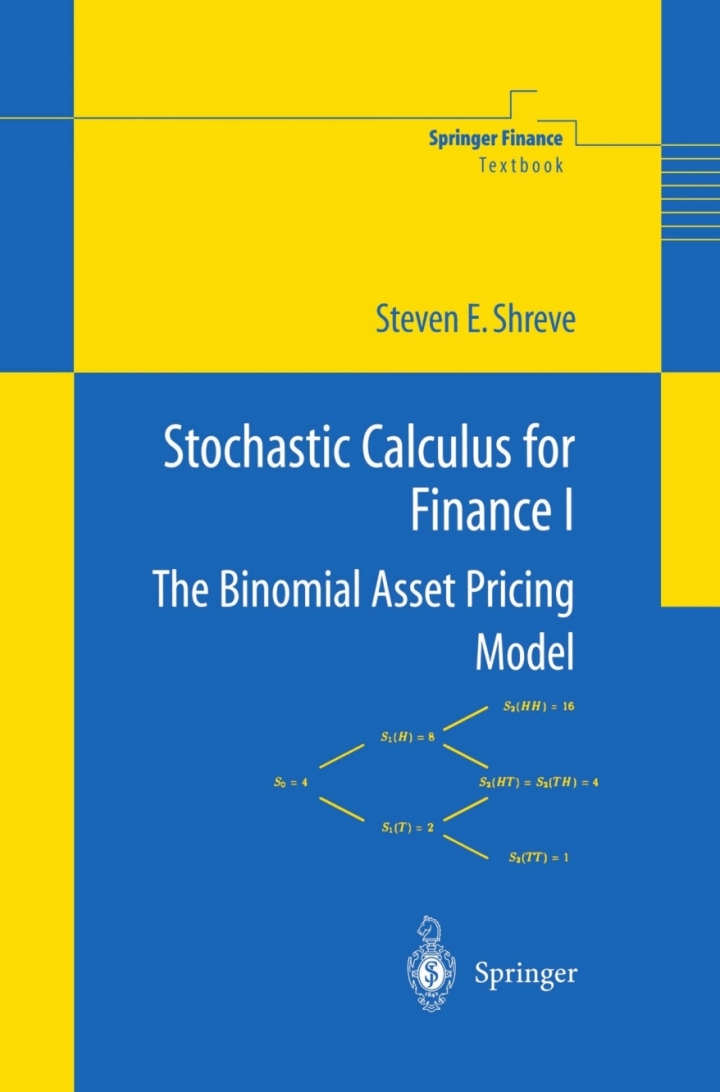

Stochastic Calculus for Finance I

Original price was: $64.99.$38.00Current price is: $38.00.

Author: Steven Shreve

Publisher: Springer

Print ISBN: 9780387249681

Delivery Time: Within 24 Hours

Copyright: 2004

500 in stock

- Save up to 60% by choosing our eBook

- High-quality PDF Format

- Lifetime & Offline Access

Stochastic Calculus for Finance I N/A

Unlock the secrets of financial modeling with ‘Stochastic Calculus for Finance I’ by Steven Shreve, a cornerstone text published by Springer. This comprehensive guide introduces essential concepts of stochastic processes tailored for finance, making it an invaluable resource for graduate students and professionals alike. With clear explanations and rigorous mathematical formulations, Shreve expertly bridges theory and practical application, covering critical topics such as Brownian motion and Ito’s lemma. Each chapter is designed to enhance understanding through well-structured examples and exercises. Elevate your financial acumen and gain a solid foundation in stochastic calculus with this must-have reference for aspiring quantitative analysts.

Note: eBooks do not include supplementary materials such as CDs, access codes, etc.